Insurance Regulations in Construction: 2026 U.S. Guide

- DJ Custom Contracting

- Jun 3

- 9 min read

Insurance regulations in construction define the mandatory coverage types, minimum limits, and contractual endorsements that contractors must maintain to comply with both legal and project-specific obligations. These rules govern general liability, workers’ compensation, and builder’s risk policies across every project type, from residential renovations to large-scale commercial builds. The standards vary significantly by state, contract, and project owner, making compliance a moving target for contractors who work across multiple jurisdictions. Understanding these requirements is not optional. It directly affects your ability to bid on projects, maintain licensing, and protect your business from catastrophic financial exposure.

What are the standard insurance requirements for construction contractors in the U.S.?

There is no federal standard for construction contractor general liability insurance. Requirements are set by state licensing boards, local jurisdictions, and individual contracts. That decentralization means a contractor licensed in New York faces different minimums than one operating in Texas or Florida.

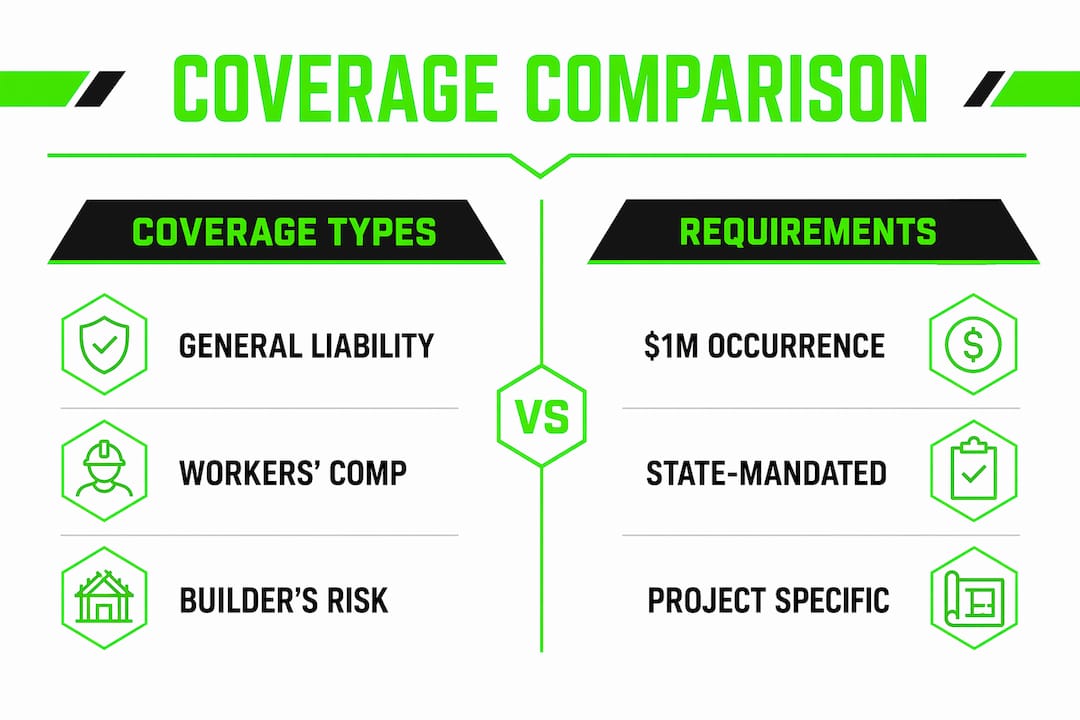

That said, commercial contracts across the U.S. consistently converge on a baseline: $1 million per occurrence and $2 million aggregate for general liability. These figures represent the floor, not the ceiling. Owners and general contractors on larger projects routinely demand $5 million or more in aggregate coverage, especially on public work or federally funded projects.

Workers’ compensation follows a similar pattern of state-by-state variation. Most states require it the moment a contractor employs even one worker. Texas is the notable exception. Texas non-subscriber general contractors face exclusion from public projects, surety bonding refusals, and unlimited tort exposure, making the opt-out a significant financial gamble in practice.

Builder’s risk insurance, also called contract works insurance, is another layer that contractors frequently overlook. Builder’s risk coverage is often contractually mandated even when no blanket state law requires it. Noncompliance can jeopardize contract award, funding disbursement, or payment milestones. For a breakdown of how these requirements differ between project types, Djcustomcontracting’s guide on residential vs. commercial construction offers useful context.

Coverage type | Typical minimum requirement | Key variation |

General liability | $1M per occurrence / $2M aggregate | Higher on public or commercial projects |

Workers’ compensation | Required in 49 states | Texas allows private employer opt-out |

Builder’s risk | Contract-specific | Triggered by project documents, not state law |

Umbrella/excess liability | $1M to $5M+ | Lender and owner-driven |

Pro Tip: Always check the insurance exhibit attached to your contract, not just the body of the agreement. Exhibits often contain higher limits and specific endorsement requirements that override general contract language.

How do endorsements and COIs impact regulatory compliance?

Certificates of insurance, commonly called COIs, are the most misunderstood documents in construction risk management. A COI proves a policy exists. It does not confer coverage rights. Misinterpreting COIs as coverage can leave parties fully exposed in litigation, even when they believed they were protected.

The actual protection comes from endorsements attached to the underlying policy. Here is what each key endorsement does and why it matters:

Additional insured (ongoing operations): Extends the subcontractor’s general liability policy to cover the general contractor or owner for claims arising from active work on the project.

Additional insured (completed operations): Extends coverage for defect claims discovered after the project is finished. Missing this endorsement leaves upstream parties vulnerable to late-discovered defect claims, which are among the most expensive in construction litigation.

Primary and noncontributory: Dictates that the subcontractor’s policy pays first. This clause prevents the hiring party from having to exhaust their own coverage before the subcontractor’s insurer responds.

Waiver of subrogation: Stops the insurer from pursuing recovery against other project parties after paying a claim. This is standard on most commercial construction contracts.

Common pitfalls include accepting a COI that lists endorsements by checkbox without verifying the actual endorsement forms. Insurance program managers verify endorsements by cross-checking form numbers and policy language directly, not by relying on ACORD form checkbox entries, which can be incomplete or inaccurate.

Pro Tip: Request the actual endorsement pages from your subcontractors’ insurers, not just the ACORD 25 certificate. Confirm the form number, edition date, and named insured language match your contract requirements exactly.

What role do state and federal policies play in shaping construction insurance rules?

The U.S. construction insurance framework is a patchwork of state laws, local licensing rules, and federal program requirements. No single federal agency sets universal construction insurance standards. That means contractors operating across state lines must track multiple regulatory regimes simultaneously.

Federal influence enters through specific programs and enforcement policies rather than blanket mandates. Four areas where federal policy directly shapes insurance expectations:

OSHA’s Multi-Employer Citation Policy allows multiple employers on a shared worksite to be cited for the same hazard. This policy affects risk management and insurance premiums by emphasizing control and reasonable protections rather than sole fault. A general contractor can be cited for a subcontractor’s safety violation if the GC had the authority to correct it.

FEMA’s Building Codes Strategy promotes adoption of hazard-resistant codes that influence insurance underwriting assumptions on construction projects. Insurers in high-risk zones increasingly price policies based on whether the project meets current FEMA-aligned code standards.

State licensing boards set minimum insurance thresholds as a condition of licensure. These minimums are often lower than what commercial contracts require, so contractors must apply whichever standard is stricter.

Public project mandates routinely impose additional requirements, including performance bonds, payment bonds, and higher liability limits, that private projects do not.

“Multi-employer OSHA citations shift risk conversations to control and prevention rather than fault, changing insurance and liability dynamics on shared worksites.” — Lancaster Safety Consulting

The practical implication is that contractors cannot rely on meeting state minimums alone. Contract documents and project-specific insurance exhibits frequently impose obligations that exceed what any licensing board requires.

How do insurance regulations influence risk management and liability?

Insurance regulations in construction do more than satisfy legal checkboxes. They set the financial boundaries of your risk exposure on every project. The coverage limits you carry define the maximum loss your insurer will absorb. Everything above those limits becomes your direct financial liability.

Endorsements are the mechanism that transfers risk to the party responsible for causing it. A properly structured additional insured endorsement, with both ongoing and completed operations coverage, means a general contractor is protected if a subcontractor’s defective work triggers a claim two years after project completion. Without it, the GC absorbs that exposure personally.

OSHA’s multi-employer enforcement adds another dimension. Even minor incidents on shared worksites can escalate premiums and affect subcontractor prequalification through the experience modification rate, known as the EMR. A higher EMR signals greater risk to insurers and owners, which can disqualify a contractor from bidding on certain projects entirely.

Insurance compliance also affects your cash flow. Contracts often tie payment milestones to proof of current coverage. If a policy lapses or a required endorsement expires mid-project, payment can be withheld until compliance is restored.

Risk factor | Impact without compliance | Impact with compliance |

General liability lapse | Contract termination, personal exposure | Continuous project eligibility |

Missing completed operations endorsement | Unprotected post-project defect claims | Full coverage through statute of repose |

High EMR from OSHA citations | Bid disqualification, premium increases | Competitive prequalification standing |

No primary/noncontributory clause | Own policy pays first on subcontractor claims | Subcontractor’s insurer responds first |

Pro Tip: Track your EMR annually. An EMR above 1.0 signals above-average risk to owners and insurers. Proactive safety programs and prompt claims reporting are the most direct tools for keeping it below that threshold.

What practical steps should contractors take for insurance compliance?

Navigating construction site insurance laws across multiple states and contracts requires a systematic approach. Reactive compliance, where you scramble to meet requirements after a contract is signed, leads to coverage gaps and delays. The following steps build a proactive compliance process:

Identify the strictest applicable standard. Compare your state licensing minimums against the contract’s insurance exhibit. Apply whichever requires higher limits or broader coverage. For contractors working in New York and New Jersey, Djcustomcontracting’s guide on insurance requirements in NY and NJ outlines the specific thresholds you need to meet.

Request full endorsement pages, not just COIs. Verify form numbers, edition dates, and named insured language against your contract requirements before work begins.

Confirm subcontractor compliance before mobilization. Flow-down requirements mean your subcontractors must carry the same endorsements you are required to provide upstream. Collect and review their endorsements, not just their certificates.

Set calendar alerts for policy expiration dates. Coverage gaps mid-project can trigger contract default provisions. Track renewal dates for every policy on the project, including subcontractors’.

Prepare separately for public project requirements. Public work often mandates performance bonds, payment bonds, and higher aggregate limits. Confirm these requirements during the bid phase, not after award.

Use certificate tracking software for multi-project or multi-state operations. Platforms designed for contractor compliance management automate expiration alerts and flag missing endorsements across your entire subcontractor roster.

The goal is a compliance posture that holds up from contract execution through the completed operations period, which can extend years beyond project closeout depending on your state’s statute of repose.

Key takeaways

Effective insurance compliance in construction requires meeting both state licensing minimums and contract-specific endorsement requirements, with endorsements carrying more legal weight than certificates of insurance.

Point | Details |

Baseline coverage minimums | General liability starts at $1M per occurrence and $2M aggregate on most commercial contracts. |

COIs vs. endorsements | Certificates prove a policy exists; endorsements determine actual coverage rights and risk transfer. |

State variation is significant | Texas allows workers’ comp opt-out, but non-subscribers lose public project eligibility and face unlimited tort exposure. |

OSHA multi-employer risk | Shared worksite citations can raise EMRs and affect subcontractor bid eligibility beyond direct claims. |

Proactive tracking matters | Monitoring policy dates, endorsement forms, and subcontractor compliance throughout the project lifecycle prevents costly gaps. |

What I’ve learned from years of managing construction insurance compliance

I have watched contractors lose project awards not because they lacked insurance, but because they submitted the wrong endorsement form. The ACORD 25 certificate looked fine. The checkbox for additional insured was checked. But when the owner’s risk manager pulled the actual endorsement, the form number was outdated and the named insured language did not match the contract. The project went to another bidder.

That scenario plays out more often than most contractors realize. The instinct is to treat the COI as the finish line. It is not. The finish line is a verified endorsement that matches the contract language word for word, with the correct form number and edition date. Anything short of that is a compliance gap waiting to surface at the worst possible moment, usually during a claim.

The OSHA multi-employer issue is another area where I see contractors underestimate their exposure. Being the controlling employer on a site means you carry citation risk for hazards you did not create. That risk feeds directly into your EMR, which feeds into your premiums and your prequalification standing. The contractors who manage this well invest in documented safety protocols and subcontractor oversight. They treat safety compliance as an insurance cost control strategy, because that is exactly what it is.

My advice: build your compliance process around endorsements, not certificates. Verify before you mobilize. Track throughout the project. And never assume that because a subcontractor handed you a COI, your coverage obligations are satisfied.

— DJ

How Djcustomcontracting delivers fully compliant construction services

Djcustomcontracting operates in full alignment with applicable local laws, licensing requirements, building codes, and construction policy guidelines on every project. Since 2018, the company has built its reputation on delivering residential and commercial work that meets the strictest insurance and regulatory standards in New York and New Jersey, protecting clients from liability exposure and keeping projects on schedule.

Whether you are planning an interior renovation, a commercial build-out, or a public works project, Djcustomcontracting carries the coverage, endorsements, and compliance documentation your project requires. Explore Djcustomcontracting’s commercial renovation services to see how a fully insured, code-compliant contractor protects your investment from day one.

FAQ

What types of insurance are required for construction contractors?

Most U.S. construction contracts require general liability, workers’ compensation, and builder’s risk insurance at minimum. Specific limits and endorsements vary by state, project type, and contract terms.

What is the difference between a COI and an additional insured endorsement?

A certificate of insurance proves a policy exists but does not grant coverage rights. An additional insured endorsement is the actual policy document that extends coverage to another party and determines their legal protections.

Are workers’ compensation requirements the same in every state?

No. Workers’ compensation is required in 49 states once an employer has employees, but Texas allows private employers to opt out. Texas non-subscribers face exclusion from public projects and unlimited tort liability exposure.

How does OSHA’s multi-employer policy affect insurance?

OSHA’s Multi-Employer Citation Policy allows multiple employers on a shared site to be cited for the same hazard. These citations can raise a contractor’s experience modification rate, increasing premiums and affecting bid eligibility on future projects.

What is primary and noncontributory coverage and why does it matter?

Primary and noncontributory is an endorsement that requires the subcontractor’s insurer to pay first on covered claims before the general contractor’s policy is triggered. Without it, a GC’s own policy may be required to contribute to losses caused by a subcontractor’s work.

Recommended

Comments