The Role of Insurance in Construction Projects

- DJ Custom Contracting

- May 31

- 8 min read

Most contractors and developers treat construction insurance as a box to check before breaking ground. That assumption creates real financial exposure. The role of insurance in construction goes far beyond paperwork. It functions as a formal mechanism for transferring financial risk from owners, contractors, and developers to insurers, and it directly shapes how projects survive unexpected setbacks. From site accidents and material losses to compliance disputes and delayed completions, the right coverage keeps projects financially viable when things go wrong. This article covers the core coverage types, how to tailor requirements to your specific project, compliance best practices, and how to treat insurance as a strategic asset.

Key Takeaways

Point | Details |

Insurance transfers financial risk | Construction insurance moves liability and loss exposure from contractors and owners to insurers through targeted policies. |

COIs are not enough | Certificates of Insurance confirm a policy exists but do not guarantee actual protection. Endorsements determine real coverage. |

Compliance requires ongoing monitoring | Policy checks at project milestones catch expiring coverage and endorsement gaps before they create liability. |

Tailor coverage to project risk | Project size, complexity, and location each affect the types and limits of coverage required for adequate protection. |

Early broker involvement pays off | Engaging an insurance broker during project planning improves underwriting terms and reduces the chance of mid-project coverage gaps. |

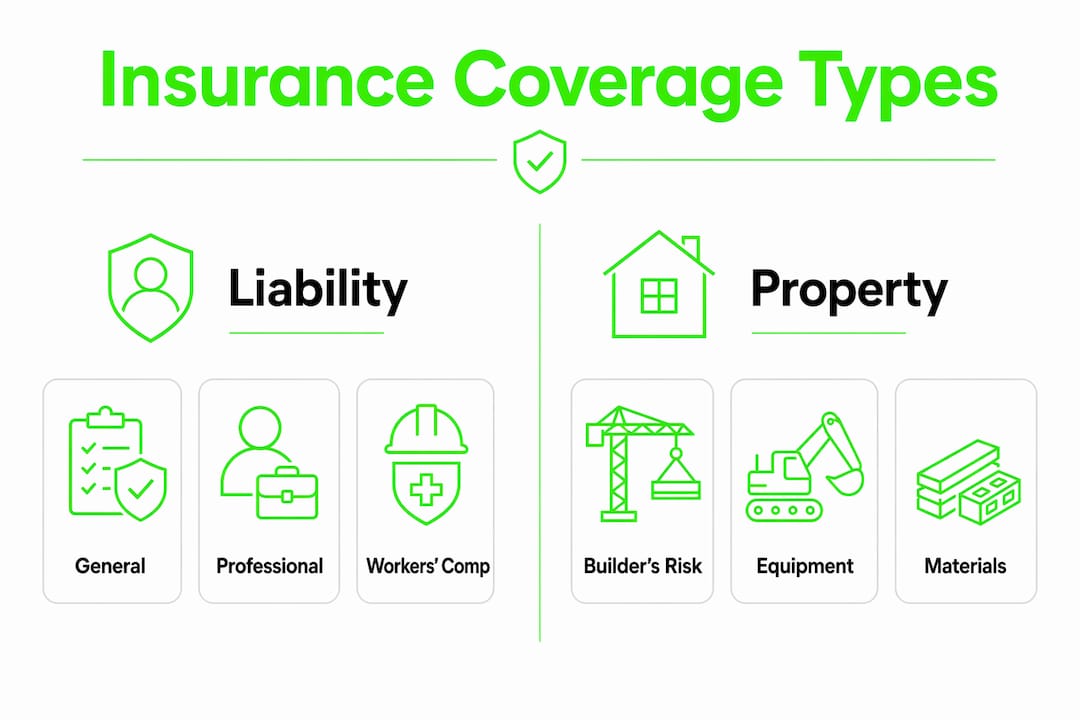

Common types of construction insurance

Understanding construction insurance starts with knowing what each policy actually covers, because construction risk management relies on combining the right policies rather than relying on a single blanket product. Each coverage type addresses a specific exposure, and the combination you need depends on your role in the project.

Coverage Type | Who It Protects | What It Covers |

General Liability | Contractors, subcontractors | Third-party bodily injury and property damage during construction |

Builder’s Risk | Owners, developers, GCs | Physical loss or damage to the structure and materials during construction |

Workers’ Compensation | Workers and employers | Medical costs and lost wages for job-site injuries |

Professional Liability (E&O) | Architects, engineers, design-build contractors | Errors or omissions in design and professional services |

Commercial Auto | Contractors with fleet vehicles | Damage and liability involving work vehicles |

Surety Bonds | Project owners | Contractor default and non-performance |

General liability is the baseline requirement on nearly every project. It covers third-party claims, including a passerby injured by falling debris or a neighboring property damaged during excavation. Most project owners and municipalities require proof of this coverage before a contractor can mobilize.

Builder’s risk operates differently. It insures structures and materials during the construction phase, but standard policies typically exclude faulty workmanship. Soft costs like delayed completion losses can be added through endorsements, which matters significantly on commercial projects with tight delivery deadlines.

Professional liability, often called errors and omissions (E&O) insurance, applies when design decisions or professional recommendations cause financial harm. For design-build contractors, this coverage fills the gap that general liability leaves open when the defect originates in the plans rather than the physical work.

Pro Tip: Never assume one policy covers everything. A contractor carrying only general liability has no protection for materials stored on site before installation. Builder’s risk fills that gap specifically.

Tailoring insurance to your project

Not every project carries the same risk profile, and applying a generic insurance template to a complex project is one of the most common and costly mistakes in construction risk management. Project size, location, site conditions, number of subcontractors, and contract structure all affect what coverage you need and how it should be structured.

Key concepts every contractor and owner should understand before finalizing insurance requirements:

Endorsements: These modify a base policy to add, remove, or change coverage. They are not optional adjustments on complex projects. They are where actual protection is defined.

Additional insured status: This extends liability protection to another party, typically the project owner or a general contractor. Without this endorsement, a subcontractor’s policy does not cover the GC if a claim arises from the sub’s work.

Waiver of subrogation: This prevents an insurer from pursuing recovery from another project party after paying a claim. It is standard language in most construction contracts and must be confirmed in the actual policy endorsement, not just the certificate.

Primary and non-contributory language: This specifies that the named contractor’s policy responds first before any other coverage the additional insured carries. Missing this language means two insurers may dispute which policy pays, delaying claims resolution.

For large infrastructure projects, engaging insurers early allows owners and brokers to negotiate customized coverage terms that reflect the specific exposures of that build. A highway interchange project carries entirely different risk than a ground-floor commercial tenant improvement. Treating them identically creates gaps.

Pro Tip: Ask your broker to review the actual endorsement forms, not just the declarations page. The declarations page summarizes the policy; the endorsements determine what it actually does.

Managing insurance compliance throughout a project

Compliance management is where many projects fall apart. Most owners and GCs collect a Certificate of Insurance at project start and file it away. That practice creates a false sense of security. COIs alone do not guarantee coverage; endorsements dictate the actual protection in place, and a COI can show active coverage while missing every critical endorsement required by the contract.

Common compliance failures and their consequences:

Missing additional insured endorsements: The GC or owner has no protection under the subcontractor’s policy if a claim arises.

Expired policies mid-project: Work performed during a lapse period creates uninsured exposure. Any claim arising during that window falls entirely on the party whose policy lapsed.

Incorrect coverage limits: A contract requiring $2 million per occurrence but backed by a $1 million policy leaves a $1 million gap the contractor must cover personally.

Missing completed operations coverage: General liability typically covers ongoing operations, but completed operations coverage extends protection after the work is finished. Many claims surface months after a project closes.

No waiver of subrogation endorsement: The insurer can pursue the GC or owner after paying a claim against the sub, which defeats the purpose of requiring the sub to carry insurance in the first place.

The solution is structured compliance checkpoints aligned to project milestones:

Pre-bid: Verify all required coverage types and limits are clearly specified in bid documents.

Pre-mobilization: Collect COIs and confirm every required endorsement is in place before any work begins.

Mid-project: Run checks at key milestones such as foundation completion, structural close-in, and MEP rough-in to catch any policy renewals or changes.

Project closeout: Confirm completed operations coverage extends at least one year beyond substantial completion.

Technology tools like automated COI tracking platforms can flag expiring policies and alert project managers before a lapse occurs. For large projects with dozens of subcontractors, manual tracking is not practical.

Workers’ compensation by state

Workers’ compensation is one area where the legal requirements are non-negotiable, and the rules vary significantly by state. Most states mandate coverage once you hire your first employee, though some states set the threshold at two, three, or more employees depending on the industry.

State Category | Requirement Trigger | Key Notes |

Most states | First employee hired | Coverage required immediately upon hiring |

Texas | Voluntary | Only state with no mandate; many clients still require it contractually |

South Dakota | Voluntary for some employers | Certain employer types are exempt |

High-risk states (e.g., NY, CA) | All employees | Strict enforcement; penalties for non-compliance are severe |

Two states stand out as exceptions. Texas does not require workers’ compensation for most employers, though contractors working on public projects or for large commercial clients often carry it anyway because client requirements frequently mandate it regardless of state law. South Dakota allows certain employers to opt out under specific conditions.

For contractors operating across state lines, each state where employees work may trigger separate coverage obligations. A New York contractor performing work in New Jersey must comply with New Jersey requirements for that project. Understanding the contractor insurance requirements in NY and NJ before mobilizing avoids costly compliance failures.

Workers’ compensation also protects employers. Without it, a single serious injury on a job site can result in a lawsuit that far exceeds the cost of the policy itself.

Integrating insurance into project governance

The strongest contractors and developers treat insurance as part of project planning from day one, not something to address after the contract is signed. Insurance functions as a strategic asset, offering access to risk engineering services, safety training, and loss control resources that directly reduce the probability and severity of claims.

Insurers are paying close attention to governance quality. Disciplined risk governance now carries significant weight in underwriting decisions for complex builds. Projects with documented safety programs, clear subcontractor qualification processes, and structured compliance monitoring receive better terms than those with none of these practices in place.

“The contractors and developers who treat insurance as an afterthought are the same ones calling their broker in a panic when something goes wrong. The ones who plan around it rarely end up in that position.”

Contractors facing rising premium costs driven by inflation, litigation trends, and weather events have an incentive beyond compliance to get this right. Strong risk controls and clean loss histories directly influence renewal pricing. A single preventable claim can raise premiums more than years of safe operations save.

When bidding on projects, your insurance program is also a statement of professionalism. Owners reviewing bids look at coverage quality, not just price. A contractor who can demonstrate robust endorsements, consistent compliance history, and early insurer engagement stands apart. Learning why hiring insured professionals matters is part of the due diligence every property owner should perform before awarding a contract.

My take on what contractors get wrong

I’ve watched contractors lose projects, face lawsuits, and pay out of pocket for situations that proper insurance would have handled. The most common mistake is not the absence of insurance. It’s the assumption that having a policy means being covered.

In my experience, the gap between what a contract requires and what the policy actually delivers comes down almost entirely to endorsements. Contractors collect a COI, hand it over, and move on. No one verifies the additional insured endorsement reflects the correct scope. No one confirms the waiver of subrogation is attached. When a claim hits, those missing pages cost far more than any premium ever would.

The other pattern I see repeatedly is treating insurance as a cost rather than a tool. Insurers offer loss control engineering, safety audits, and site assessment resources that most contractors never use. Those services exist because insurers want to prevent claims. Taking advantage of them reduces your exposure and signals to the underwriter that you are a disciplined operation worth backing at reasonable rates.

My advice is simple. Bring your broker into the project planning process early. Make compliance monitoring a scheduled task, not a reactive one. And read the endorsements.

— DJ

Work with a contractor who takes compliance seriously

At Djcustomcontracting, insurance compliance and risk management are part of every project, not an afterthought. Founded in 2018, the company has built a reputation for delivering residential and commercial construction work that meets all applicable licensing, building code, and insurance requirements. Whether you need a commercial renovation contractor with documented compliance practices or an interior renovation specialist who understands the role of insurance in renovations and what it means to protect your investment, Djcustomcontracting brings the experience and accountability your project deserves. No job too big, no job too small.

FAQ

What does construction insurance actually cover?

Construction insurance is a collection of policies covering third-party liability, physical damage to structures and materials, worker injuries, professional errors, and contractor default. The specific protection depends on which policies are in place and how they are endorsed.

Why are endorsements more important than a Certificate of Insurance?

A Certificate of Insurance confirms a policy exists but does not guarantee coverage. Endorsements modify the policy to include critical protections like additional insured status, waiver of subrogation, and primary and non-contributory language. Without the right endorsements, the COI is largely meaningless.

When should workers’ compensation insurance be secured?

Most states require workers’ compensation as soon as you hire employees, with Texas and South Dakota as the primary exceptions. Even in voluntary states, contractors often secure coverage early because project owners and clients frequently require it contractually before allowing work to begin.

How often should insurance compliance be checked during a project?

Compliance should be verified at structured milestones including pre-bid, pre-mobilization, key mid-project phases, and project closeout. Policies can expire or change mid-project, and proactive monitoring at milestones prevents gaps that create uninsured exposure.

Does builder’s risk insurance need to be extended if a project runs long?

Yes. Builder’s risk policies are written for a specific project duration, and if the project exceeds that timeline, the policy must be extended to maintain continuous coverage. Failing to extend leaves the project uninsured during the remaining construction period.

Recommended

Comments