What Are Insurance Regulations: A 2026 Guide

- DJ Custom Contracting

- a few seconds ago

- 7 min read

Insurance regulations are state-based legal frameworks designed to ensure insurance companies operate fairly, remain financially solvent, and protect consumers from unfair practices. Understanding what are insurance regulations matters directly to property owners, business operators, and contractors, because non-compliance can halt projects, void coverage, and trigger penalties. The McCarran-Ferguson Act of 1945 established that states, not the federal government, hold primary authority over insurance oversight. The National Association of Insurance Commissioners (NAIC) supports this system by developing model laws that states may adopt and adapt.

What are insurance regulations and how does the U.S. system work?

The United States operates a decentralized, state-based system with 50 independent Departments of Insurance, each holding authority over licensing, rate filings, market conduct, and solvency within its borders. That structure means a contractor or business owner operating in New York faces different rules than one operating in Texas or California. Federal law steps in only when a state fails to regulate insurance or when Congress explicitly legislates for the industry.

The NAIC functions as a coordinating body, not an enforcement authority. It develops model laws covering solvency standards, claims handling procedures, and licensing requirements. Those models become enforceable only after a state legislature adopts them, and states routinely modify the language before passage. That gap between NAIC guidance and actual state law is where most compliance confusion originates.

State insurance commissioners carry the real regulatory power. They approve or reject rate filings, license insurers and agents, investigate market conduct complaints, and initiate enforcement actions. Two common rate approval systems exist across states:

Prior approval: The insurer must receive commissioner sign-off before a new rate takes effect.

File and use: The insurer files the rate and may use it immediately, subject to later review.

Pro Tip: Check your state’s Department of Insurance website directly for the rate system in effect. The NAIC’s consumer information portal lists each state’s approach and current commissioner contact details.

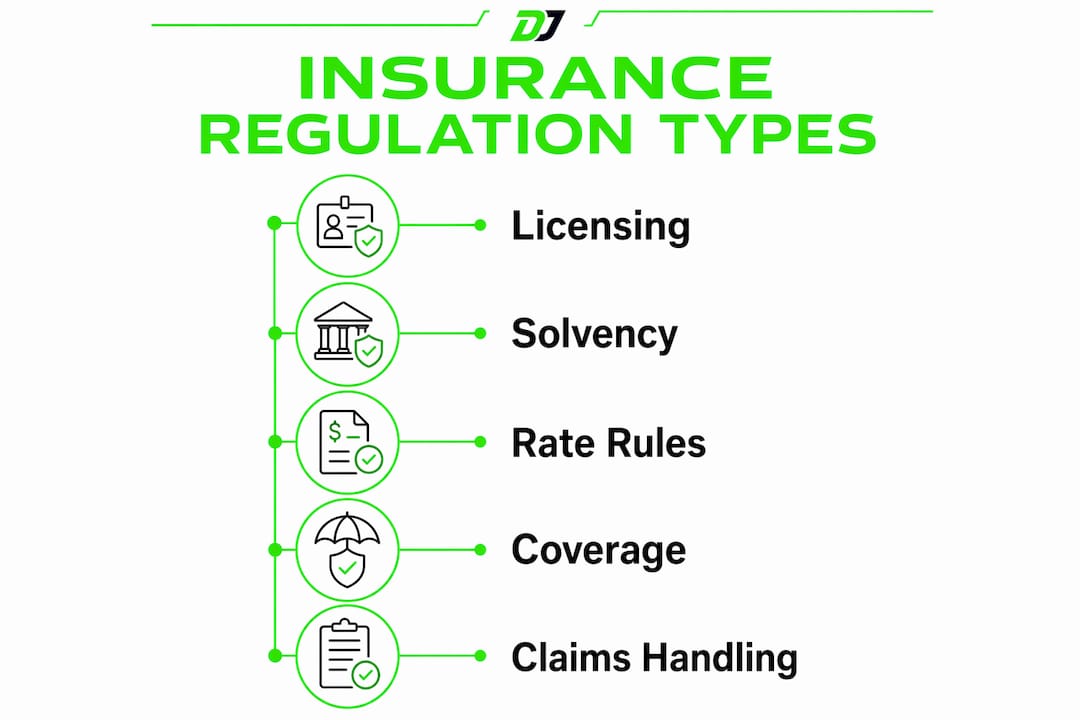

Major types of insurance regulations affecting property and business owners

Insurance regulation covers several distinct categories, each with direct consequences for property owners and business operators.

Licensing and certificates of authority

Every insurer selling policies in a state must hold a certificate of authority issued by that state’s Department of Insurance. Buying coverage from an unlicensed carrier can leave you without legal recourse if a claim is denied. Agents and brokers also carry individual licensing requirements, which vary by state and line of insurance.

Solvency and financial reserve standards

Regulators require insurers to maintain adequate financial reserves to pay future claims. Insurers demonstrate this through statutory financial filings, including compliance with the NAIC Model Audit Rule. A carrier that cannot meet reserve thresholds faces regulatory intervention, which can include supervised rehabilitation or liquidation. For policyholders, this is the mechanism that protects your claim payment even when an insurer faces financial stress.

Rate adequacy rules

Regulators prohibit rates that are excessive, inadequate, or unfairly discriminatory. Excessive rates harm consumers. Inadequate rates threaten insurer solvency. Unfairly discriminatory rates treat similar risks differently without actuarial justification. These three standards appear in virtually every state’s insurance code.

Mandatory coverage requirements

Certain coverages are legally required for businesses. Workers’ compensation insurance is mandatory in nearly every state for employers with employees. General liability insurance is required for licensed contractors in most jurisdictions. The table below summarizes the most common mandatory coverage categories:

Coverage Type | Who It Applies To | Regulatory Basis |

Workers’ compensation | Employers with employees | State labor and insurance codes |

General liability | Licensed contractors and businesses | State contractor licensing laws |

Surety bonds | Public works contractors | Miller Act (federal) and state equivalents |

Professional indemnity | Consultants and design professionals | State licensing boards and new 2025 statutes |

Market conduct and claims handling

State insurance departments enforce market conduct rules by reviewing consumer complaints and auditing insurer practices. Penalties range from fines to full license suspension or revocation. This enforcement track gives property owners and business operators a direct, non-litigation path to recourse when a carrier mishandles a claim.

How do insurance regulations apply to contractors and construction?

Construction is one of the most heavily regulated industries from an insurance standpoint. The role of insurance regulations in construction goes beyond basic policy procurement. It connects directly to licensing, permit issuance, and contract eligibility.

General liability insurance. Most states require licensed contractors to carry general liability coverage before a license is issued or renewed. A lapsed policy can trigger immediate license suspension.

Workers’ compensation. In California, all licensed contractors must carry workers’ compensation regardless of employee count as of 2026. Similar mandates exist across most states. Missing this coverage is one of the fastest routes to a work stoppage.

Surety bonds. Public works projects commonly require surety bonds under the Miller Act, which guarantees project completion and payment to subcontractors. State equivalents apply to public projects below the federal threshold.

Professional indemnity. From july 1, 2025, new statutory requirements impose professional indemnity insurance obligations on contractors and consultants, including coverage for directors and employees. These mandates may apply retrospectively, meaning existing projects could fall under new coverage thresholds.

DOB and permit compliance. In New York and New Jersey, the Department of Buildings ties permit issuance directly to verified insurance certificates. A contractor without current, compliant coverage cannot pull permits, which stops a project before it starts.

Pro Tip: Review your policy’s coverage exclusions every time a new project begins. Legislative changes to construction insurance obligations can apply to active contracts, not just new ones. Proactive review prevents gaps that only surface at claim time.

Insurance requirements in construction often exceed minimum legal mandates to address project-specific risks. Owners and general contractors routinely require subcontractors to carry higher limits than state law demands. Understanding the difference between the legal floor and the contractual requirement protects both parties.

What business owners must know about staying compliant

Insurance compliance is not a one-time event. It is a continuous process that requires monitoring financial health, tracking regulatory updates, and confirming that coverage aligns with current legal requirements.

Key compliance responsibilities for business owners include:

Multi-state mapping. If your business operates across state lines, NAIC model laws must be mapped to each state’s specific statutes. Adoption varies widely, and what satisfies one state may not satisfy another.

Ongoing statutory filings. Insurers and large self-insured businesses must submit regular financial reports. Missing a filing deadline can trigger regulatory scrutiny even when the underlying financials are sound.

License and certificate renewals. Insurance licenses for carriers and agents expire. A lapsed certificate of authority means the insurer cannot legally write new policies in that state.

Monitoring regulatory updates. State legislatures amend insurance codes regularly. Subscribing to your state Department of Insurance’s bulletin service is the most direct way to catch changes before they affect your coverage.

Choosing compliant policies. Work with a licensed broker who specializes in your industry. For contractor insurance in NY and NJ, state-specific requirements differ enough that a generalist broker may miss critical coverage gaps.

The consequences of non-compliance are concrete. State departments can revoke licenses, issue stop-work orders, and impose fines. For contractors, a single missing policy can halt an entire project and expose the business owner to personal liability.

Key Takeaways

Insurance regulations are state-based legal frameworks enforced by individual Departments of Insurance, and compliance requires continuous monitoring of coverage, filings, and regulatory updates across every state where you operate.

Point | Details |

State authority governs insurance | The McCarran-Ferguson Act gives each state independent power over insurance licensing, rates, and solvency. |

NAIC model laws guide but don’t enforce | States adopt NAIC models with modifications; compliance requires mapping to each state’s actual statutes. |

Contractors face layered requirements | General liability, workers’ compensation, surety bonds, and professional indemnity are all legally required in most jurisdictions. |

Non-compliance stops work | Missing a required policy or filing can result in license suspension, permit denial, or a full project work stoppage. |

Compliance is ongoing | Regulatory updates, policy renewals, and statutory filings require active monitoring, not a one-time policy purchase. |

Why I treat insurance compliance as a non-negotiable part of every project

Most contractors think about insurance the way they think about a fire extinguisher. You get it, you put it on the wall, and you hope you never need it. That mindset is exactly what gets projects shut down.

What I have seen working in residential and commercial contracting since 2018 is that the gap between having insurance and being compliant is wider than most owners realize. A policy that satisfied your licensing board last year may not meet the coverage thresholds required by a new contract or a new state statute this year. Legislative changes, especially the professional indemnity mandates that took effect in 2025, can apply to projects already underway. That is not a hypothetical. It is a real exposure that most contractors discover only after a claim is denied.

The NAIC’s coordinating role is genuinely useful, but it creates a false sense of uniformity. I have worked on projects spanning multiple states and the differences in how states adopt model laws are significant. What counts as adequate general liability coverage in one jurisdiction may fall short in another. The only reliable approach is to verify requirements state by state, not assume that one compliant policy covers all operations.

The practical lesson is this: treat insurance compliance as part of your project planning, not an afterthought. Confirm coverage before pulling permits. Review exclusions before signing contracts. And when regulations change, reassess your existing policies immediately rather than waiting for renewal.

— DJ

Djcustomcontracting keeps your project compliant from start to finish

Djcustomcontracting has operated as a licensed general contractor since 2018, delivering residential and commercial projects in full accordance with applicable insurance regulations, building codes, and licensing requirements.

Every project Djcustomcontracting takes on is backed by verified general liability coverage, workers’ compensation, and the documentation required by local Departments of Buildings. Whether you need commercial renovation services that meet current regulatory standards or a contractor who understands the permit and insurance requirements specific to New York and New Jersey, Djcustomcontracting brings the compliance knowledge and trade experience to protect your investment. Contact Djcustomcontracting to discuss your project and confirm that every regulatory requirement is covered before work begins.

FAQ

What are insurance regulations in simple terms?

Insurance regulations are state-established rules that govern how insurance companies operate, including how they price policies, handle claims, and maintain financial reserves to pay policyholders.

Which federal law gives states authority over insurance?

The McCarran-Ferguson Act of 1945 grants states primary authority to regulate and tax insurance, with federal law applying only when states fail to regulate or Congress explicitly legislates for the industry.

What insurance does a contractor legally need?

Most states require contractors to carry general liability insurance and workers’ compensation as conditions of licensing. Public works projects also require surety bonds under the Miller Act or state equivalents.

What happens if a contractor does not have required insurance?

State departments can suspend or revoke a contractor’s license, deny permit applications, and issue stop-work orders. Missing coverage also exposes the business owner to direct personal liability on a project.

How do I stay current on insurance regulation changes?

Subscribe to your state Department of Insurance’s bulletin service and review your policies at the start of each project. For construction-specific updates, the 2026 construction regulatory guide covers current requirements for contractors operating in the U.S.

Recommended