Contractor insurance requirements in NY and NJ: Essential guide

- DJ Custom Contracting

- May 13

- 9 min read

Many contractors assume that holding a general liability policy and handing over a certificate of insurance (COI) covers every compliance requirement on a project. In New York and New Jersey, that assumption can be dangerously expensive. The type of coverage, minimum dollar amounts, required forms, endorsement wording, and registration rules vary by state, city, contract, and trade. A single gap in any of those layers can halt a permit application, void a contract, or leave you personally exposed to a claim. This guide breaks down exactly what you need to carry, prove, and document to stay compliant and competitive in the NY/NJ market.

Table of Contents

Key Takeaways

Point | Details |

Know required insurance types | Contractors in NY and NJ typically need general liability and workers’ compensation and must often provide specialized proof for both. |

Mind city and state rules | Local regulations and state mandates may require different forms, amounts, and recent registration steps. |

HIC program specifics in NJ | NJ home improvement contractors must meet strict registration and insurance proof standards, often exceeding $500,000 coverage per occurrence. |

Endorsement wording matters | Project contracts’ ‘additional insured’ language can expand or restrict coverage and is a frequent source of disputes. |

Compliance is workflow | Staying compliant means systemizing renewals, verifying forms, and not assuming one COI or insurance policy is always enough. |

Understanding the basics: What insurance is required?

With foundational misconceptions addressed, let’s clarify exactly which types of insurance matter and for whom.

Most contractors working in New York or New Jersey need to maintain at least four types of coverage. Each serves a different legal and contractual function, and they are not interchangeable.

Commercial General Liability (CGL): Covers third-party bodily injury and property damage arising from your operations. It is the policy most clients and agencies request first.

Workers’ Compensation: Covers your employees if they are injured on the job. This is a statutory requirement, not optional, in both states.

Disability Benefits Insurance: Required separately in New York (and distinct from workers’ comp). It covers non-work-related illness or injury for employees.

Commercial Automobile Liability: Required any time a vehicle is used in business operations, whether owned, leased, or hired.

The insurance requirements for building permits in New York make clear that applicants must provide proof of Commercial General Liability insurance and, separately, Workers’ Compensation coverage. These are treated as independent filings, not a single combined certificate.

Requirements also shift based on who you are working for. On federal contracts, FAR clauses can require contractors to maintain all four types above, sometimes with specified minimum limits that exceed state thresholds. Employer headcount also matters. Some statutory obligations only kick in once you employ a certain number of workers, while others apply from day one.

“The specific form of proof required is just as important as the policy itself. A compliant policy submitted on the wrong document is still a non-compliant submission.”

Understanding remodeling compliance in NY and NJ means knowing that these baseline requirements are the floor, not the ceiling. Contract terms and local agency rules frequently raise them.

Pro Tip: Request a copy of the actual endorsements on your policy, not just the declarations page. Endorsements are where the real coverage details live, and they are what agencies and general contractors scrutinize most closely.

New York contractor insurance: State, city, and recent registration changes

Now that the basic types of insurance are covered, let’s zoom in on New York’s multi-agency compliance maze, including the most recent regulatory changes.

New York operates on multiple compliance levels simultaneously: state law, city-specific rules, and agency-level requirements at the Department of Buildings (DOB). Each layer can add requirements beyond what the others mandate.

What NYC’s DOB actually requires

According to guidance on NYC DOB insurance requirements, many DOB-licensed contractors must carry General Liability with a minimum of $1 million per occurrence. Beyond the dollar amount, the DOB requires specific forms for Workers’ Compensation and Disability Benefits. Generic ACORD certificates are not accepted as substitutes for these forms. The required documents include:

C-105.2 — Certificate of Workers’ Compensation Insurance

U-26.3 — Certificate of Workers’ Compensation Insurance (for self-insured employers)

DB-120.1 — Certificate of Disability Benefits Insurance

Submitting the wrong form, even with the correct underlying policy in place, results in a rejected application. That kind of clerical error has stopped projects in their tracks for weeks.

The 2024 statewide registration layer

New York also added statewide contractor registration requirements starting December 30, 2024. This is an additional compliance step on top of local licensing and permit requirements. General contractors and subcontractors working in New York now need to register at the state level, which includes submitting proof of insurance that meets specific statewide thresholds. This is not the same as a NYC DOB license, and having one does not satisfy the other.

NYC vs. state: A quick comparison

Requirement | NYC DOB | NY State (Post-Dec. 2024) |

CGL minimum | $1M per occurrence | State-set minimum (varies by trade) |

Workers’ comp proof form | C-105.2 or U-26.3 | State-accepted forms |

Disability benefits form | DB-120.1 | DB-120.1 |

ACORD certificates accepted | No (for WC/DB) | Varies by agency |

Statewide registration required | No (separate DOB license) | Yes |

When navigating selecting a Manhattan contractor or pulling permits for a residential project, understanding this dual-track system is not optional. It is the difference between a smooth submission and a delayed start date. For residential additions specifically, review the NYC addition permit steps to understand how insurance filings integrate into the full permit workflow.

Pro Tip: Create a document folder for each project that includes the exact certificate forms required by that specific agency. Do not reuse a COI from a prior project without confirming the form type matches the current requirement.

New Jersey contractor insurance: Home improvement and trade-specific compliance

Turning to New Jersey, the insurance landscape changes, especially if you perform home improvement or specialized trade work. Here is how the requirements break down.

New Jersey’s primary framework for residential contractors is the Home Improvement Contractor (HIC) registration program. If you perform residential work valued at over $500, registration is required. That registration is not purely administrative. It carries insurance obligations tied to New Jersey’s Consumer Fraud Act framework, and the NJ HIC registration requirements are specifically designed to protect consumers from unlicensed and underinsured contractors.

CGL minimums and workers’ comp thresholds

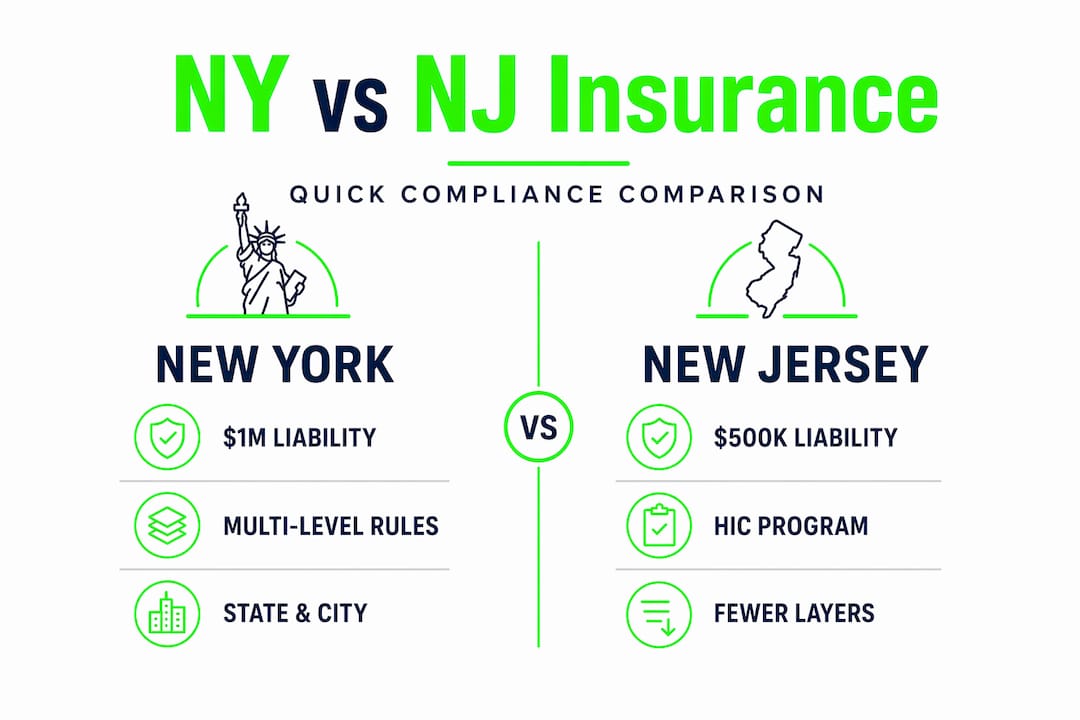

Under the HIC framework, New Jersey requires a minimum Commercial General Liability coverage of $500,000 per occurrence, as referenced under N.J.S.A. 56:8-151. That is half of NYC’s DOB threshold, but it is the floor. Many general contractors and developers in New Jersey require subcontractors to carry $1 million or more per occurrence in their contract terms, regardless of what state law mandates.

For workers’ compensation, New Jersey requires coverage for any employer with at least one employee. There is no minimum headcount exception. Failure to maintain coverage triggers significant financial penalties, and repeat violations can result in criminal charges. Unlike some states where sole proprietors have flexibility, New Jersey treats this seriously from the first hire.

NY vs. NJ insurance comparison

Requirement | New York | New Jersey |

CGL minimum (state/city) | $1M per occurrence (NYC DOB) | $500K per occurrence (HIC) |

Workers’ comp trigger | Employees required | 1 or more employees |

Disability benefits | Required (DB-120.1) | Not a separate state requirement |

Registration program | NY State (Dec. 2024) + NYC DOB license | HIC registration (NJDCA) |

Residential work threshold | Permit-based | Over $500 in value |

Trade licenses in New Jersey (electrical, plumbing, HVAC) may add insurance requirements on top of HIC registration, with some boards setting their own minimums.

Proof of insurance must typically be submitted during registration renewal, not just at initial application.

Lapses in coverage, even brief ones, can result in registration suspension.

For residential work, reviewing NJ home renovation essentials provides context on how insurance requirements fit into the broader project planning process for bathroom and interior renovation projects.

Pro Tip: If you are a subcontractor working under a general contractor in New Jersey, verify that your own HIC registration and insurance are current. The general contractor’s coverage does not extend to you automatically.

Contractual requirements and endorsement pitfalls: Additional insured status

State-mandated insurance is only half the battle. Contractual obligations often drive the actual coverage risks and disputes that contractors face.

Providing a COI to a general contractor or project owner is a routine step on any project. What most contractors do not fully appreciate is that the COI itself is not coverage. It is merely evidence that coverage exists. The actual protection depends entirely on the endorsements attached to the policy and the specific wording those endorsements use.

Why additional insured endorsements matter

When a contract requires you to name another party as an additional insured, that party gains certain rights under your policy. But the scope of those rights depends on the endorsement language. ISO additional insured endorsements differ in scope, and those differences can materially affect coverage outcomes, often becoming the source of major disputes.

Two phrases that appear in endorsement wording can mean entirely different things in practice:

“Arising out of” — Broader language. The additional insured is covered for a wider range of claims connected to your work, even if you were only partially involved.

“Caused, in whole or in part” — More restrictive. Coverage applies only where your direct actions contributed to the loss.

This distinction becomes critical when a third-party injury claim involves multiple parties. If the endorsement uses “caused, in whole or in part” but the contract required “arising out of,” there is a coverage gap, and the dispute often ends up in litigation.

Practical checklist for subcontractors reviewing contracts

Before signing any subcontract, verify the following:

Does the contract require you to add the GC and/or owner as additional insureds?

What endorsement form does your policy currently use, and does it match the contract requirement?

Does the additional insured requirement apply to completed operations, not just ongoing work?

Is the certificate holder listed correctly, with the exact legal entity name?

Is the endorsement actually attached to the policy, or just referenced on the COI?

“A certificate of insurance that lists someone as a certificate holder does not make them an additional insured. Only a policy endorsement does that. These are not the same thing, and confusing them is one of the most common and costly errors in construction contracting.”

When planning project compliance from the start, reviewing contract insurance language before mobilization avoids the kind of disputes that unwind projects mid-construction.

What most compliance articles miss about contractor insurance

Here is the perspective that rarely makes it into a standard compliance guide: the contractors who get into the most trouble with insurance are not the ones who skipped buying coverage. They are the ones who bought the right policy and then treated it as a completed task.

Insurance compliance is not a one-time event. It is a workflow. Policies renew annually. Endorsements can change at renewal without triggering a notification to the policyholder. A certificate that was valid when submitted for a permit may have expired by the time an inspection occurs. If the renewal was not coordinated with the DOB filing or the project owner, you are technically operating without compliant coverage, even though you have been paying premiums the whole time.

The real differentiator in this industry is operational discipline. The contractors who build a renewal calendar, who confirm endorsement language every time they sign a new subcontract, and who maintain a project-specific insurance file are the ones who avoid costly delays. The ones who assume their broker handles everything, or that last year’s COI still works this year, are the ones facing stop-work orders.

Building that discipline does not require a large administrative team. It requires a consistent process. Review your endorsements quarterly. Confirm your certificate forms meet the specific agency requirements for every active project. Never let a renewal pass without confirming that all named additional insureds are still correctly listed on the updated policy.

For those managing residential additions in the city, the NYC home addition compliance checklist is a useful companion to the insurance review process, connecting permit steps with the documentation requirements that run parallel to them.

The contractors who treat insurance as a living part of their operations, not a box checked at project start, are the ones who finish jobs without interruption.

Stay compliant and build with confidence

Navigating insurance requirements across New York and New Jersey takes more than a policy document. It takes a contractor who understands the rules and has built compliance into their process from the ground up.

At DJ Custom Contracting LLC, every project we take on is fully insured in accordance with applicable state, city, and contractual requirements. Whether you are managing a general contracting project in New York or New Jersey or planning a complex interior renovation, our team carries the right coverage and maintains the documentation to prove it at every stage. We work with residential and commercial clients across the region and are equipped to handle projects where insurance and permit compliance are non-negotiable. Reach out to discuss your next project and work with a contractor who has the paperwork, the coverage, and the experience to back it up.

Frequently asked questions

What is the minimum general liability insurance for contractors in NYC?

NYC generally requires at least $1 million per occurrence for general liability insurance, and the DOB mandates specific certificate forms rather than standard ACORD certificates for certain coverages.

Are workers’ compensation and disability benefits both required for New York contractors?

Yes. New York requires both coverages separately, and contractors must submit specific state-issued forms such as C-105.2 and DB-120.1 rather than a generic certificate of insurance.

What is the minimum insurance for New Jersey home improvement contractors?

Home improvement contractors in New Jersey must maintain at least $500,000 per occurrence in commercial general liability coverage under the HIC registration program, as referenced in N.J.S.A. 56:8-151.

When does a contractor need workers’ compensation in New Jersey?

Any New Jersey contractor with at least one employee must carry workers’ compensation insurance, with no minimum headcount exception and significant penalties for noncompliance.

How do contractual additional insured requirements impact coverage?

The specific endorsement wording used determines the actual scope of coverage. ISO endorsement language differences such as “arising out of” versus “caused, in whole or in part” can be the deciding factor in whether a claim is covered or disputed.

Recommended

Comments